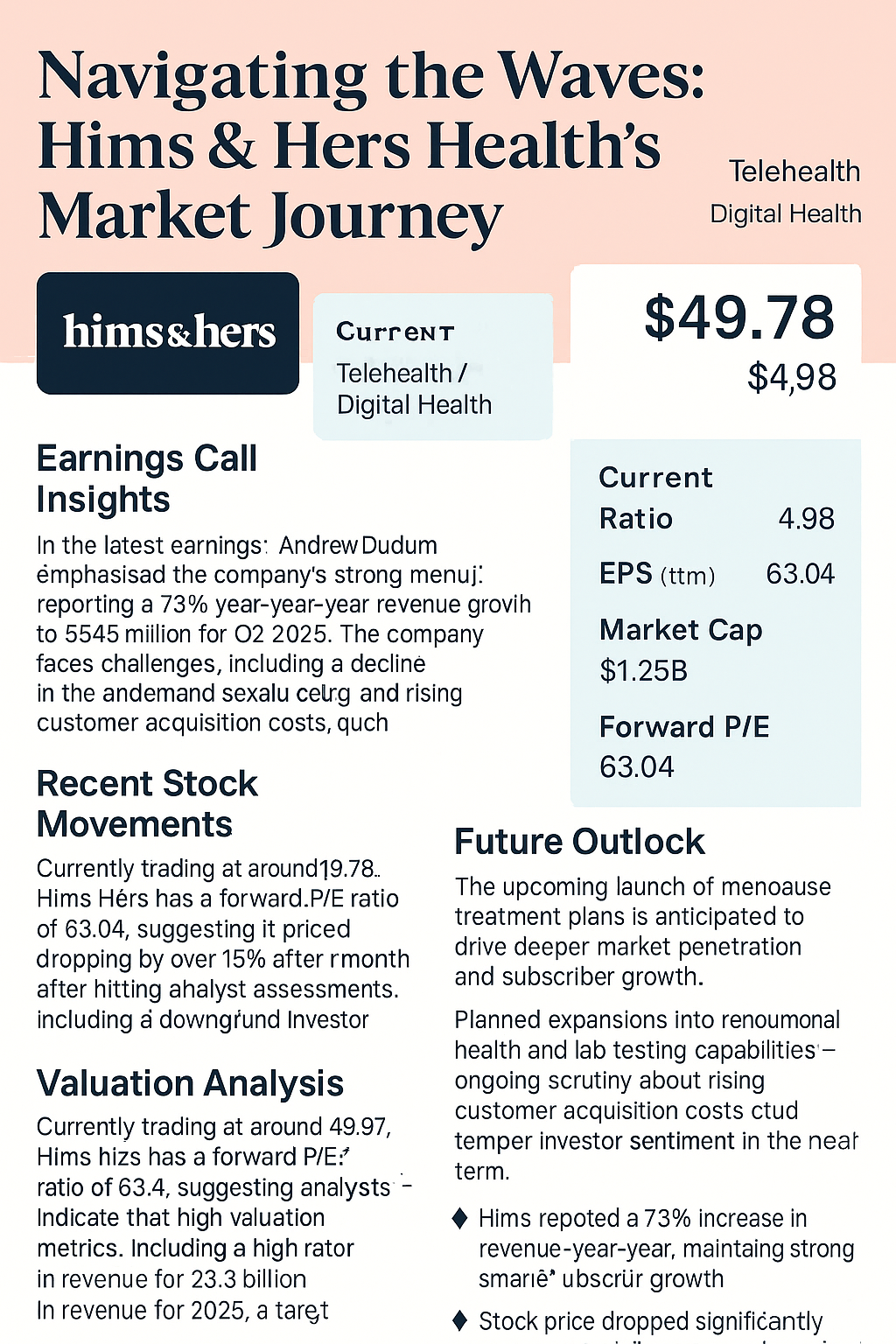

Earnings Call Insights

In the latest earnings call, Hims & Hers CEO Andrew Dudum emphasized the company’s strong momentum, reporting a 73% year-over-year revenue growth to $545 million for Q2 2025. The platform now serves over 2.4 million subscribers, illustrating the growing demand for personalized healthcare solutions. However, the company faces challenges, including a decline in the on-demand sexual health segment and rising customer acquisition costs, which could impact future profitability.

Recent Stock Movements

Hims & Hers has seen significant stock price fluctuations recently, with shares dropping by over 15% after hitting a 52-week high earlier in the month. This volatility followed mixed analyst assessments, including a downgrade from Bank of America, which cited concerns about third-quarter sales. Yet, despite these challenges, the stock remains up approximately 135% year-to-date, reflecting investor optimism about its long-term growth potential.

Valuation Analysis

Currently trading at around $49.78, Hims & Hers has a forward P/E ratio of 63.04, suggesting it is priced for significant growth compared to its peers. However, analysts indicate that the high valuation metrics, including a PEG ratio of 4.04, may deter value investors, especially with Zacks ranking it a #4 (Sell). Looking ahead, the company aims for over $2.3 billion in revenue for 2025, a target that could enhance its valuation if met.

Future Outlook

The upcoming launch of menopause treatment plans is anticipated to drive deeper market penetration and subscriber growth. With planned expansions into hormonal health and lab testing capabilities, Hims & Hers is positioning itself to become a comprehensive provider of personalized healthcare. However, ongoing scrutiny about rising customer acquisition costs and competition in the telehealth space could temper investor sentiment in the near term.

Data‑driven notes on equities. No hype—just facts, charts, and context.